1. r*

= − (1/θ) M/P + γ/θ −

τ + (ε/θ) Y

2. Y

= ( a + δ

+ ΦBT + DSB)/(s + m)

− μ/(s + m) r*

+ m*/(s + m) Y*

− σ/(s + m) Q

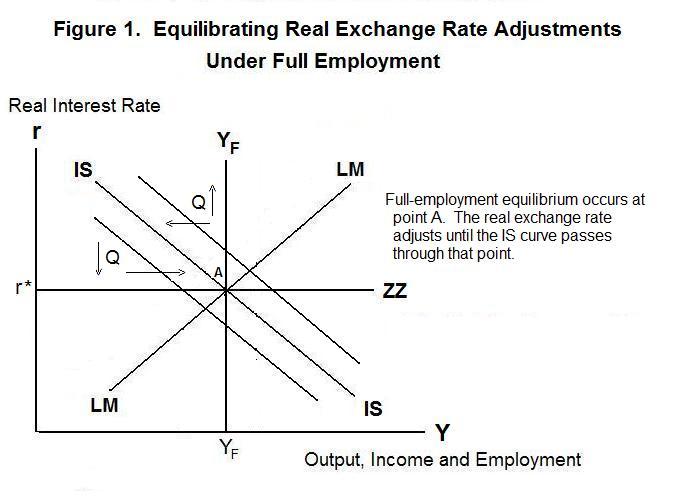

Equations 1 and 2 appear as the LM and IS curves respectively in

Figure 1. The vertical line YF specifies the full-employment

level of output and the horizontal line ZZ specifies that the domestic real

interest rate is determined by world market conditions at r*.

We now extend our analysis to focus on the situation of full-employment.

For full-employment to be continuously maintained, the price level must

adjust freely in response to market forces. We assume that the exchange

rate, as before, is allowed to float freely in response to the forces of supply

and demand in the foreign exchange market. As you should now know, the small

open economy is in equilibrium when both stock (asset market) and flow (real

goods market) equilibrium hold. We begin by reproducing the equations of stock

and flow equilibrium.

The IS curve gives the combinations of income and the real interest rate for which the aggregate quantity of domestic output that world residents wish to purchase equals the quantity produced. An increase in the world real interest rate causes a reduction in desired domestic investment leading to an upward movement along the curve and a decline in real income. A rise in the real exchange rate shifts domestic and foreign demand off domestic goods causing the desired current account balance to deteriorate and the IS curve to shift to the left---a smaller level of domestic income is now associated with each level of the world interest rate. An exogenous increase in desired consumption or investment, increase in desired exports, or reduction in desired imports shifts IS to the right.

The LM curve gives the combinations of income and the world real interest rate for which desired money holdings equal actual holdings and, hence, desired aggregate non-monetary asset holdings equal actual holdings. A rise in the interest rate, holding M/P constant, reduces desired money holdings and requires an increase in income to increase them back to their initial level---the LM curve is thus positively sloped. An increase in the real money supply (increase in M or fall in P) requires a higher level of real income to produce an equivalent increase in desired money holdings at a constant world interest rate---LM thus shifts to the right. An exogenous increase in desired real money holdings has the opposite effect. An increase in the expected inflation rate reduces desired money holdings at each level of r* and Y , shifting LM to the right.

Full-employment equilibrium requires that the IS and LM curves cross the vertical YF line at the same point. Moreover, this point must be consistent with the world real interest rate determined independently of what is happening in the domestic economy. We represent this world interest rate by the horizontal line ZZ. When there is full-employment equilibrium, therefore, the intersection of the IS and LM curves must occur where YF and ZZ cross. Endogenous variables must adjust to drive the IS and LM curves through this equilibrium (r* , Y) combination, denoted as point A.

We established earlier that the real exchange rate must adjust to maintain output at YF, given the world real interest rate. If IS crosses ZZ at an output level above full employment more domestic output will be demanded than is being produced. The relative price of domestic output, Q, must rise to choke off this excess demand, shifting the IS curve to the left until it passes through the point A. A rise in the equilibrium real exchange rate can take place through either a rise in either the price level P or fall in the nominal exchange rate Π. (Recall that the real exchange rate is equal to P / Π P*.) Which variable will adjust in this case--- P or Π ?

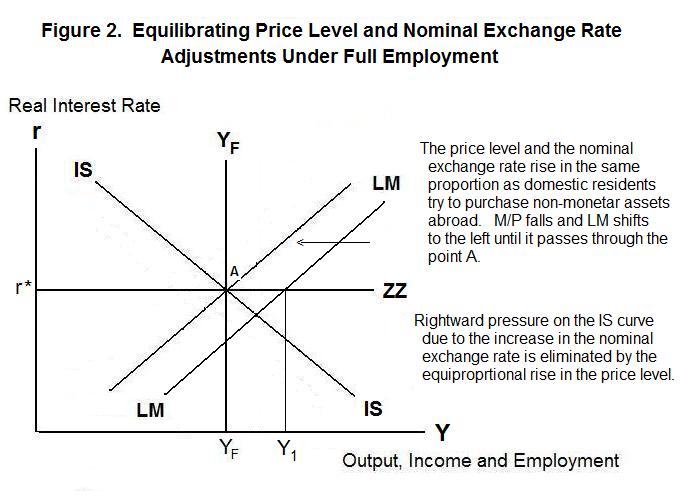

Suppose that Q has adjusted so that IS crosses ZZ at the point A but that, as shown in Figure 2, the LM curve crosses the ZZ line at a level of income Y1 above full employment. Income would have to rise to Y1 to make domestic residents willing to hold the existing money stock---they have excess money holdings at YF . Domestic residents are out of portfolio equilibrium and will buy non-monetary assets with their excess money holdings. Since all domestic residents want to increase their asset holdings, assets will have to be purchased from foreign residents. This will create an excess supply of domestic currency on the world market, causing the price of foreign currency in terms of domestic currency Π to rise---that is, the nominal value of the domestic currency to fall.

At a given domestic price level P the rise in Π will reduce the relative international price of domestic goods, Q , and shift world demand onto domestic output. This will result in rightward pressure on the IS curve. To the extent that IS tries to move to the right beyond the intersection at point A, however, there will be excess demand for goods and services. The price level P will be bid up until Q and IS have returned to their original levels, making the demand for domestic goods again consistent with domestic full-employment output. As P rises domestic residents' real money holdings will decline, shifting the LM line to the left. This adjustment process will continue as long as domestic residents have excess money holdings---that is, until LM crosses ZZ at the point A.

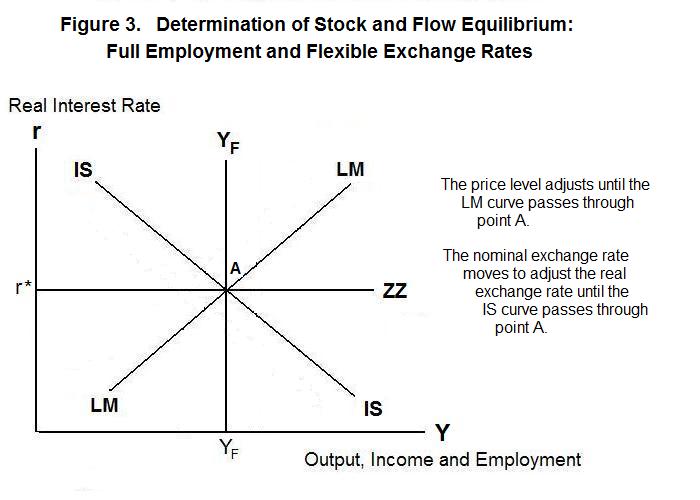

This answers the question of whether the adjustment of Q will occur through changes in P or changes in Π . The price level will adjust until domestic residents are in portfolio equilibrium, shifting the LM curve until it crosses through the equilibrium point A. As this happens, the nominal exchange rate will also adjust, changing the real exchange rate and shifting the IS curve until it too crosses through point A. This is illustrated in Figure 3.

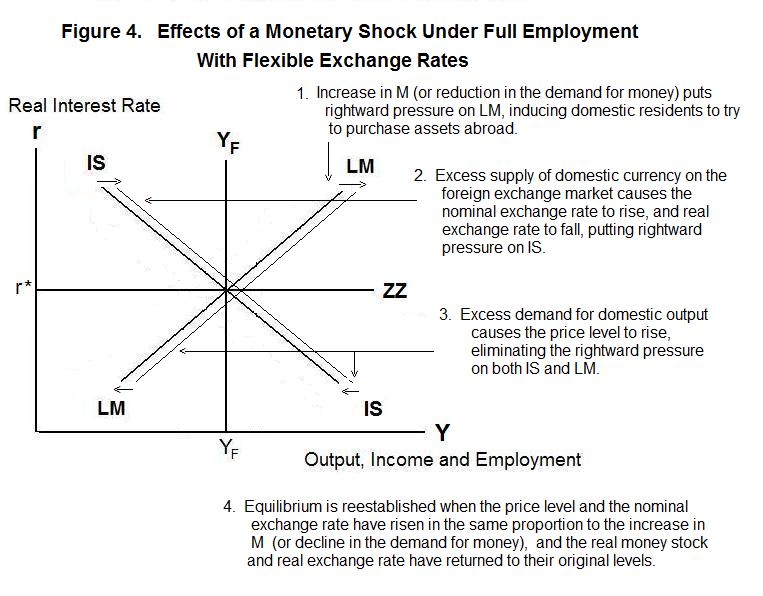

Suppose that, starting from a position of full-employment equilibrium, the government increases the domestic nominal money supply. This will create excess money balances in the hands of domestic residents, putting rightward pressure on the LM curve in Figure 4 and leading domestic residents to attempt to purchase assets abroad. The resulting excess supply of domestic currency on the international market will cause it to depreciate (Π to rise) which will create excess aggregate demand for domestic output and lead to an increase in the price level. Ultimately, the domestic price level will rise in proportion to the increase in the nominal money supply so that M/P will return to its original level. And Π will rise in proportion to the increases in P (and M) to maintain Q at its original level. The LM and IS curves will thus return to their initial positions. No actual net purchases of assets by domestic residents from abroad will occur---the change in the price level will return real money holdings to their old level, at which no increase in holdings of non-monetary assets will be required. Similarly, no actual switch of world expenditure onto domestic goods will take place since the real exchange rate (relative price of domestic goods) will also return to its old level.

This idea that changes in the nominal money supply will lead to proportional changes in nominal prices and the nominal exchange rate, leaving real money holdings, the real exchange rate and real income unaffected is called the neutrality of money. Money is neutral (under full employment conditions) in that it has no effect on real magnitudes. Only nominal values change.

It is test time again! As usual, be sure and think up your own answers before looking at the ones provided.

Question 1

Question 2

Question 3

Choose Another Topic in the Lesson.