To simplify the exposition it will be incorrectly assumed that the United States

comprises one-half of the world economy. The model will also be based on the

assumption that the other countries in the world can be aggregated into a

composite economy that is identical in structure to the United States and that

all countries in this composite respond identically to changes in U.S. policy.

The analysis will be constructed within an IS-LM framework. The IS curve

represents the combinations of real income and the real interest rate associated with flow

equilibrium in the country's market for real goods and services. It is negatively

sloped because a fall in the real interest rate will lead to an increase in y the

price of capital goods relative to other goods in the economy, making it profitable

to expand the capital stock by increasing the level of domestic investment. In the

short run when the price level is unaffected, this expansion of investment will lead

to an increase in the equilibrium level of output and employment. The IS curve will

shift to the right as a result of a devaluation of the domestic real exchange rate

with respect to the rest of the world.

The LM curve represents the combinations of real income and the real interest rate

associated with stock equilibrium of the country's asset market. This equilibrium

occurs when the demand for domestic real money balances equals the supply---if

residents have their desired holdings of money, they must also have their desired

aggregate holdings of non-monetary assets. While the analysis focuses on the

real interest rate relevant for domestic investment in the economy as a whole, there

will be a whole structure of equilibrium interest rates on the individual assets in the

aggregate for which the existing mix of those assets is willingly held. The LM curve

is positively sloped because a rise in the real interest rate reduces desired holdings

of domestic real money balances, requiring a higher level of real income to equivalently

increase desired money holdings so that the existing domestic real money stock is willingly

held. An increase in the supply of money, or reduction in demand for it, shifts the LM

curve to the right.

Since world output is the sum of the output of the countries that make up that world, the

world IS and LM curves will be the horizontal sums of the IS curves of those individual

countries. This is portrayed in Figures 1, 2 and 3 below, where the United States is

represented by country B and the rest-of-world aggregate is represented by country A and

a unit of output on the horizontal axis in the world panel equals two units of output

on the horizontal axes on the panels representing each of the two countries. Assuming that

the U.S. and the rest of the world are the same size, rightward shifts of the IS and LM

curves of country A or country B will produce a rightward shift of the world IS or LM of

half their magnitude. The interest rates in both parts of the world equal the world

interest rate and the labeled vertical lines in the three panels represent the full-employment

levels of output.

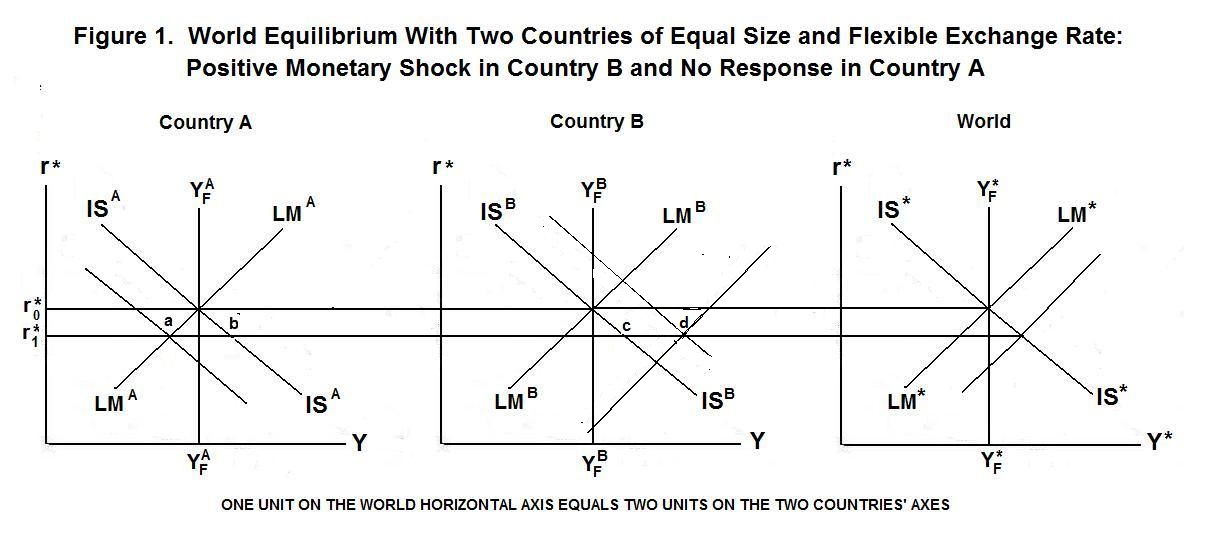

Now let us begin the analysis by assuming that the U.S., represented by Country B in

Figure 1 below, increases its money supply, shifting LM{B} to the right

by the amount shown on the graph and the world LM curve, LM{*} , to the

right by half that magnitude. That is, a two percent increase in the U.S. money supply will

represent a one percent increase in the world money supply.

The presentation that follows analyses the effects of United States monetary

policy on output and employment in the rest of the world as well as in the

United States. The effects on other countries will depend upon how their

monetary authorities respond to the domestic consequences of changes in U.S.

monetary policy.

The world interest rate falls from r{0}{*} to r{1}{*} . Given the initial level of the exchange rate and the underlying price levels, stock equalibrium in the U.S. will occur at point d and flow equilibrium will occur at point c. The excess money holdings of U.S. residents will lead them to purchase assets abroad, creating an excess supply of the domestic currency in the world market and a decline in the country's nominal and real exchange rates which will shift world demand off foreign and onto U.S. goods, shifting the IS{B} curve to the right to pass through point d. This real exchange rate shift will also shift IS{A} to the left by the same amount so that it passes through point a in the left-most panel, ensuring that rest-of-world stock and flow equilrium both occur at the output associated with point a.

The effect of the U.S. monetary expansion is clearly an increase in U.S. output at the expense of output in the rest of the world. The fall in the world interest rate in the absence of the change in the real exchange rate has the effect of increasing U.S. output to point c and rest-of-world output to point b while the associated devaluation of the U.S. dollar further increases U.S. output to point d while eliminating the increase in rest-of-world output that resulted from the fall in the interest rate and further reducing that output to point a.

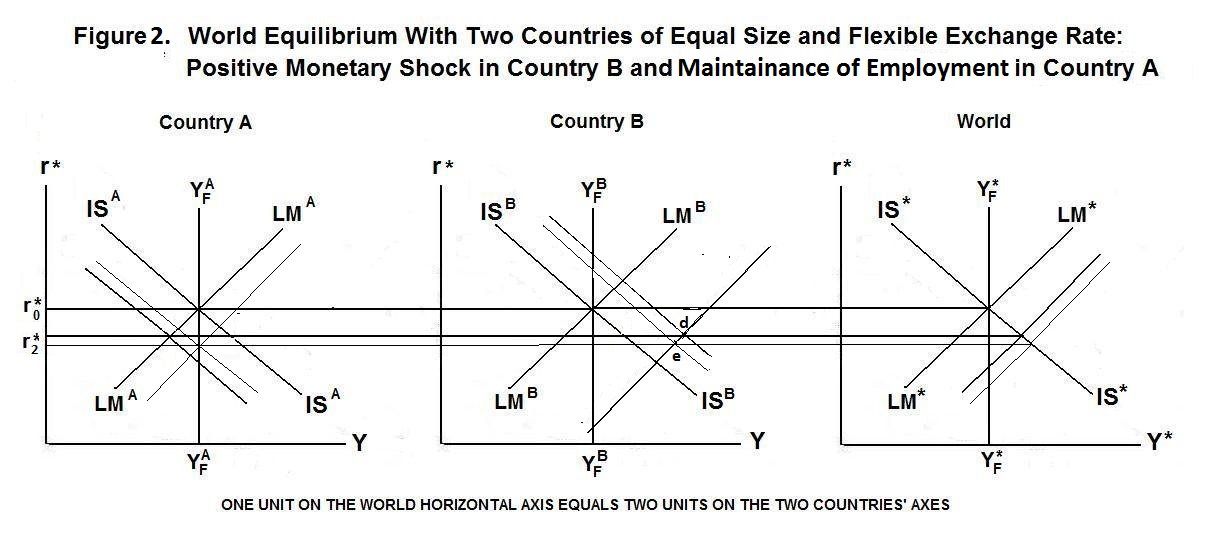

The above analysis assumes that the monetary authorities in the rest of the world do nothing to offset the effects on their output and employment of the expansionary U.S. monetary policy. Suppose, instead, that they increase their domestic money supplies sufficiently to maintain output at the full-employment level. This is shown in Figure 2 below.

The rightward shift of the LM curve in the rest of the world also shifts the world LM curve to the right by half that amount, further reducing the world interest rate to r{2}* . This monetary expansion appreciates the U.S. dollar, shifting IS{B} to the left to pass through the new world interest rate at point e with an equivalent rightward shift of IS{A} to pass through the intersection of the new rest-of-world LM curve with the new world interest rate and the vertical full-employment line. A rest-of-world policy of maintaining domestic output in the face of the the U.S. monetary expansion thus moderates somewhat the effect of that expansion on U.S. output and employment.

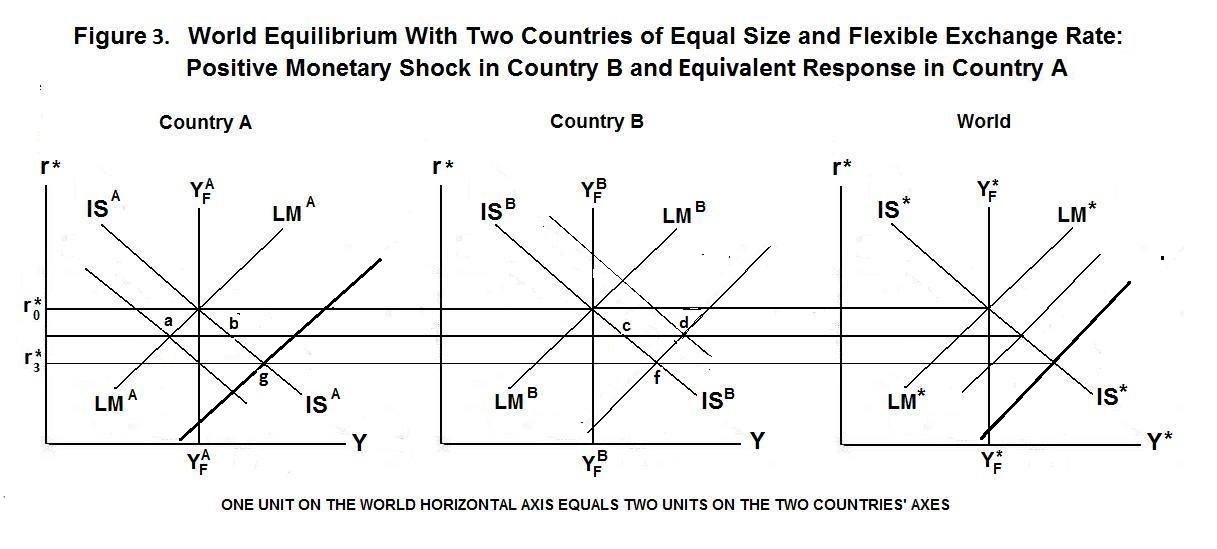

It is also possible that the authorities in the rest of the world, being aware of the effect of the appreciation of their currencies with respect to the U.S. dollar, and unaware of the exact degree of domestic monetary expansion necessary to maintain domestic output and employment, would simply expand their money supplies sufficiently to offset the appreciation of their exchange rates. This is shown in Figure 3 below.

The rest-of-world LM curve shifts to the right by the same amount as the U.S. LM curve and the world LM curve also ends up shifting by the same amount. These LM curves are shown by the thick dark lines in Figure 3. The world interest rate falls to r{3}* and output and employment expand by the same amount throughout the world---that is to point f in the United States and point g in the rest-of-world aggregate. Since there is no change in exchange rates, IS curves both in the U.S. and abroad remain unchanged. In effect, the United States is running world monetary policy!

The question arises as to what happens in the long-run when wages and prices are flexible. In all three cases above, the rise in the price level offsets the money-supply induced shift in the LM curve and no changes in output and employment in the U.S. or abroad can arise. If only the U.S. money supply expands, the U.S. price level will rise in proportion to that expansion and the U.S. dollar will fall in nominal value in the same proportion with real exchange rates remaining unchanged. Since there is no effect on output and employment in the rest of the world, there is no reason for those countries to modify their money supplies and their price levels will remain constant. Were these rest-of-world authorities to expand their money supplies to keep their domestic currencies from appreciating in terms of the U.S. dollar, their price levels will rise in proportion to the U.S. price level.